Knowledge Center

Why Diversification Matters

Key takeaways

- Diversification can help manage risk.

- You may avoid costly mistakes by adopting a risk level you can live with.

- Rebalancing is a key to maintaining risk levels over time.

One way to balance risk and reward in your investment portfolio is by diversifying your assets.

Diversification is the practice of spreading your investments around so that your exposure to any one type of asset is limited. This practice is designed to help reduce the volatility of your portfolio over time.

One of the keys to successful investing is learning how to balance your comfort level with risk against your time horizon. Invest your retirement nest egg too conservatively at a young age, and the growth rate of your investments may not keep pace with inflation. Conversely, if you invest too aggressively when you're older, you could leave your savings exposed to market volatility, which could erode the value of your assets at an age when you have fewer opportunities to recoup your losses.

You can balance risk and reward in your investment portfolio by diversifying your assets. At its root, this strategy is the simple idea of spreading your portfolio across several asset classes. Diversification can help mitigate the risk and volatility in your portfolio, potentially reducing the number and severity of stomach-churning ups and downs. Remember, diversification does not ensure a profit or guarantee against loss.

The primary components of a diversified portfolio

Domestic stocks

Stocks represent the most aggressive portion of your portfolio and provide the opportunity for higher growth over the long term. However, this greater potential for growth carries a greater risk, particularly in the short term. Because stocks are generally more volatile than other types of assets, your investment in a stock could be worth less when you decide to sell it.

Bonds

Most bonds provide regular interest income and are generally considered to be less volatile than stocks. They can also act as a cushion against the unpredictable ups and downs of the stock market, as they often behave differently than stocks. Investors who are more focused on safety than growth often favor US Treasury or other high-quality bonds, while reducing their exposure to stocks. These investors may have to accept lower long-term returns, as many bonds—especially high-quality issues—generally don't offer returns as high as stocks over the long term. However, note that some fixed income investments, like high-yield bonds and certain international bonds, can offer much higher yields, but with more risk.

Short-term investments

While the RPB Plan does not offer them, these include money market funds and short-term CDs (certificates of deposit). Money market funds are conservative investments that offer stability and easy access to your money. They usually provide lower returns than bond funds or individual bonds. While money market funds are considered safer and more conservative, they are not insured or guaranteed by the Federal Deposit Insurance Corporation (FDIC) the way many CDs are.1 When you invest in CDs though, you may sacrifice the liquidity generally offered by money market funds.

The primary short-term investment option in the RPB Plan is the RPB Capital Preservation Fund. This fund is considered a stable value fund, which is a portfolio of bonds that are insured to protect the investor against a decline in yield or a loss of capital. The owner of a stable value fund will continue to receive the agreed-upon interest payments regardless of the state of the economy. Also available is the Vanguard Short-Term Bond Fund, which is the lowest volatility of the standalone bond funds available in our Tier 2.

International stocks

Stocks issued by non-US companies often perform differently than their US counterparts, providing exposure to opportunities not offered by US securities. If you're searching for investments that offer both higher potential returns and higher risk, you may want to consider adding some foreign stocks to your portfolio.

Real estate funds

Real estate funds, including real estate investment trusts (REITs), can also play a role in diversifying your portfolio and providing some protection against the risk of inflation.

Target allocation funds

For investors who don't have the time or the expertise to build a diversified portfolio, target allocation funds can serve as an effective single-fund strategy. RPB manages five target allocation funds, each of which maintain a specific asset allocation based on conservative, moderate, and aggressive risk profiles.

How diversification can help reduce the impact of market volatility

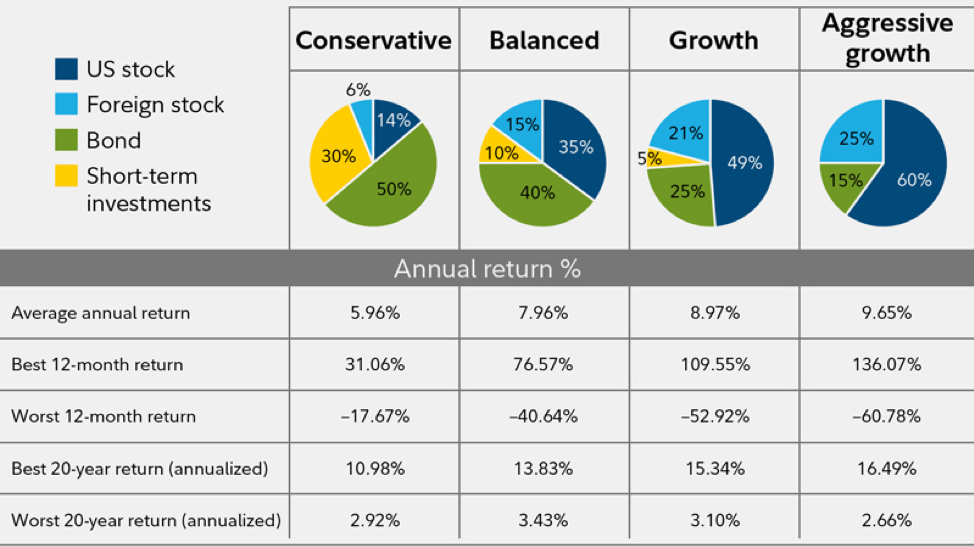

The primary goal of diversification isn't to maximize returns. Its primary goal is to limit the impact of volatility on a portfolio. To better understand this concept, look at the chart below, which depict hypothetical portfolios with different asset allocations. The average annual return for each portfolio from 1926 through 2015, including reinvested dividends and other earnings, is noted, as are the best and worst 20-year returns.

The most aggressive portfolio shown comprises 60% domestic stocks, 25% international stocks, and 15% bonds: it had an average annual return of 9.65%. Its best 12-month return was 136%, while its worst 12-month return would have lost nearly 61%. That's probably too much volatility for most investors to endure.

Changing the asset allocation slightly, however, tightened the range of those swings without giving up too much in the way of long-term performance. For instance, a portfolio with an allocation of 49% domestic stocks, 21% international stocks, 25% bonds, and 5% short-term investments would have generated average annual returns of almost 9% over the same period, albeit with a narrower range of extremes on the high and low end. As you can see when looking at the other asset allocations, adding more fixed income investments to a portfolio will slightly reduce one’s expectations for long-term returns, but may significantly reduce the impact of market volatility. This is a trade-off many investors feel is worthwhile, particularly as they get older and more risk-averse.

(Note: This chart represents hypothetical portfolios. The asset allocations do not represent those of any RPB funds, and are not a predictor of future returns.)

Factoring time into your diversification strategy

People are accustomed to thinking about their savings in terms of goals: retirement, college, a down payment, or a vacation. But as you build and manage your asset allocation—regardless of which goal you're pursuing—there are two important things to consider. The first is the number of years until you expect to need the money—also known as your time horizon. The second is your attitude toward risk—also known as your risk tolerance.

For instance, think about a goal that's 25 years away, like retirement. Because your time horizon is long, you may be willing to take on additional risk in pursuit of long-term growth, under the assumption that you'll usually have time to regain lost ground in the event of a short-term market decline. In that case, a higher exposure to domestic and international stocks may be appropriate.

But here's where your risk tolerance becomes a factor. Regardless of your time horizon, you should only take on a level of risk with which you're comfortable. So even if you're saving for a long-term goal, if you're more risk-averse you may want to consider a more balanced portfolio with some fixed income investments. And regardless of your time horizon and risk tolerance, even if you're pursuing the most aggressive asset allocation models, you may want to consider including a fixed income component to help reduce the overall volatility of your portfolio.

The other thing to remember about your time horizon is that it's constantly changing. So, let's say your retirement is now 10 years away instead of 25 years—you may want to reallocate your assets to help reduce your exposure to higher-risk investments in favor of more conservative ones, like bond or money market funds. This can help mitigate the impact of extreme market swings on your portfolio, which is important when you expect to need the money relatively soon.

Once you've entered retirement, a large portion of your portfolio should be in more stable, lower-risk investments that can potentially generate income. But even in retirement, diversification is key to helping you manage risk. At this point in your life, your biggest risk is outliving your assets. So just as you should never be 100% invested in stocks, it's probably a good idea to never be 100% allocated in short-term investments if your time horizon is greater than one year. After all, even in retirement you will need a certain exposure to growth-oriented investments to combat inflation and help ensure your assets last for what could be a decades-long retirement.

Regardless of your goal, your time horizon, or your risk tolerance, a diversified portfolio is the foundation of any smart investment strategy.

- You could lose money by investing in a money market fund. Although the fund seeks to preserve the value of your investment at $1.00 per share, it cannot guarantee it will do so. The Fund may impose a fee upon the sale of your shares or may temporarily suspend your ability to sell shares if the Fund’s liquidity falls below required minimums because of market conditions or other factors. An investment in the fund is not insured or guaranteed by the Federal Deposit Insurance Corporation or any other government agency. Fidelity Investments and its affiliates, the fund’s sponsor, have no legal obligation to provide financial support to the fund, and you should not expect that the sponsor will provide financial support to the fund at any time.

- Asset mix performance figures are based on the weighted average of annual return figures for certain benchmarks for each asset class represented. Historical returns and volatility of the stock, bond, and short-term asset classes are based on the historical performance data of various indexes from 1926 through the most recent year-end data available from Morningstar. Domestic stocks represented by S&P 500 1926 – 1986, Dow Jones U.S. Total Market 1987– most recent year end; foreign stock represented by S&P 500 1926 – 1969, MSCI EAFE 1970 – 2000, MSCI ACWI Ex USA 2001 – most recent year end; bonds represented by U.S. intermediate-term bonds 1926 – 1975, Barclays U.S. Aggregate Bond 1976 – most recent year end; short term represented by 30-day U.S. Treasury bills 1926 – most recent year end. It is not possible to invest directly in an index. Although past performance does not guarantee future results, it may be useful in comparing alternative investment strategies over the long term. Performance returns for actual investments will generally be reduced by fees and expenses not reflected in these investments’ hypothetical illustrations. Indexes are unmanaged. Generally, among asset classes, stocks are more volatile than bonds or short-term instruments and can decline significantly in response to adverse issuer, political, regulatory, market, or economic developments. Although the bond market is also volatile, lower-quality debt securities, including leveraged loans, generally offer higher yields compared with investment-grade securities, but also involve greater risk of default or price changes. Foreign markets can be more volatile than U.S. markets due to increased risks of adverse issuer, political, market, or economic developments, all of which are magnified in emerging markets.